Construction Coverage – a leading online publisher of construction industry research reports – has released the 2026 edition of the hottest real estate markets in the United States, revealing where demand is still surging despite a national cooldown.

While home sales are down 8.3% year over year and price growth has slowed to just 1.1%, certain markets remain highly competitive, with homes selling quickly and often above asking.

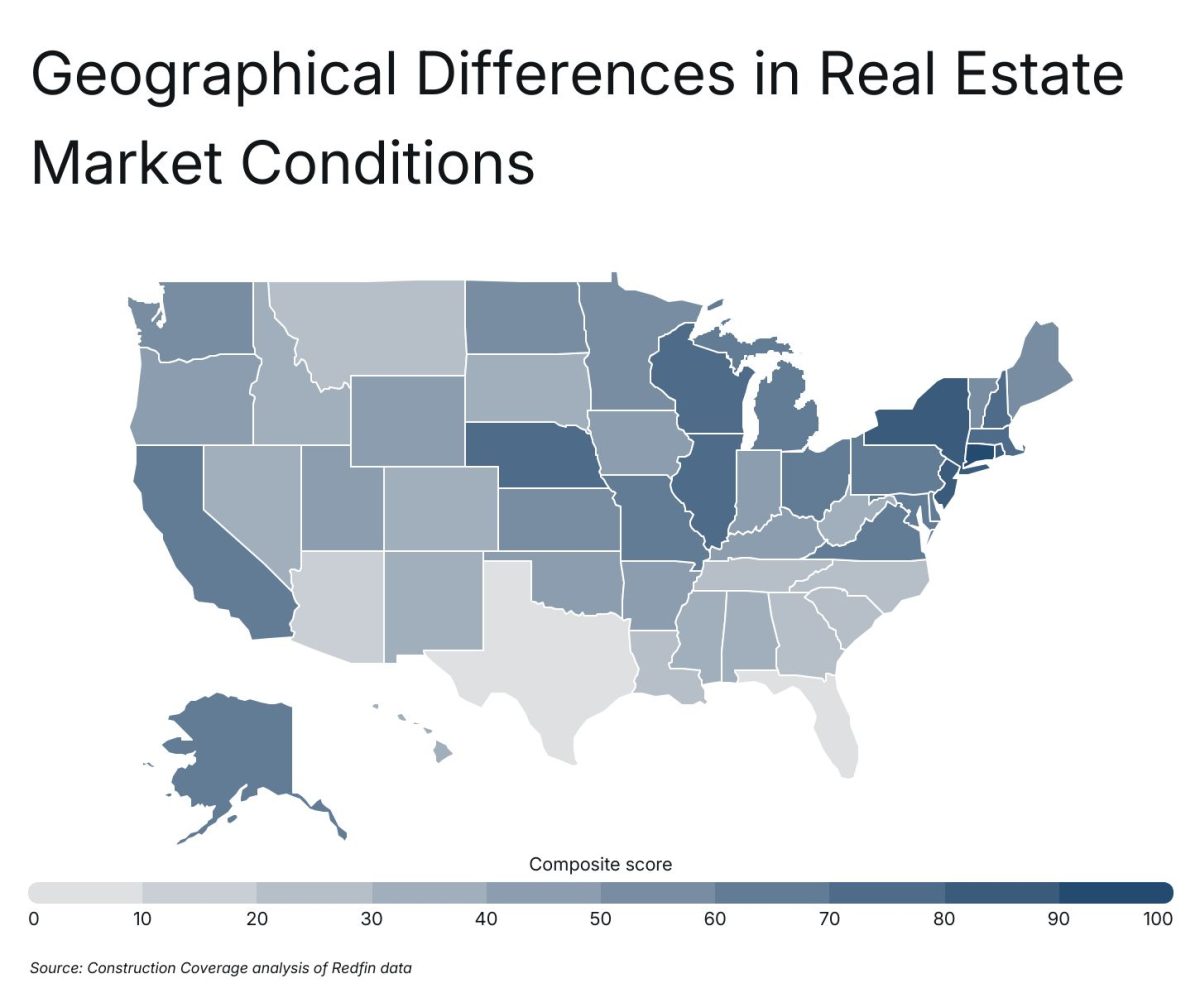

States in the Northeast dominate the rankings, with seven in the top 10. Connecticut leads the country with a composite score of 93.9, followed closely by New Jersey (89.0), Rhode Island (87.8) and New York (86.9). Here it’s interesting to note that New York City, the hub of three of these states, ranks only 21st among the hottest markets/large cities, due in part to high prices, which may help explain the appeal of the tristate as a whole. Among the 850 hot urban real estate markets cited, three are Big Apple suburbs in our coverage area — Stamford (No. 4), White Plains (14) and New Rochelle (17).

Rounding out the top 10 states are Massachusetts, Wisconsin, Illinois, New Hampshire, Nebraska and Pennsylvania.

Here is the data for Connecticut:

- Composite score: 93.9

- Median sale price (January 2026) – $446,400;

- One-year change in median sale price (2024–2025) – +7.3%;

- Share of homes that sold above asking – 56.2%;

- Median number of days on the market – 38.3;

- Average sale-to-list percentage – 102.3%;

- Share of listings with price drops – 17.7%.

And New York state:

- Composite score: 86.9;

- Median sale price (January 2026) – $601,100;

- One-year change in median sale price (2024–2025) – +6.6%;

- Share of homes that sold above asking – 41.6%;

- Median number of days on the market – 39;

- Average sale-to-list percentage – 101.1%;

- Share of listings with price drops – 19.9%.

For comparison, here are the statistics for the United States:

- Composite score – not applicable;

- Median sale price (January 2026) – $422,921;

- One-year change in median sale price (2024–2025) – +1.6%;

- Share of homes that sold above asking – 27.0%;

- Median number of days on the market – 48.7;

- Average sale-to-list percentage – 98.8%;

- Share of listings with price drops – 18.1%.

Slower sales, higher prices locally

The national picture dovetails with the local one. In the first quarter of 2026, the Westchester, Putnam and Dutchess counties real estate markets demonstrated resilience despite mixed market conditions, according to the recently released Houlihan Lawrence Q1 2026 Westchester-Putnam-Dutchess Market Report. https://issuu.com/houlihanlawrence/docs/houlihan_lawrence_q1-2026_westchester_putnam_dutch While transaction volume softened in certain areas, the report continued, pricing remained strong across all three counties, driven by ongoing inventory constraints and steady buyer demand.

Westchester saw a slowdown in sales activity, with a 16% decrease in homes sold year over year. Despite this, home values continued to rise, with the average sale price reaching $1.3 million, up 11%. Inventory remains limited, and demand continues to outpace supply across most price points, highlighting sustained competition among buyers.

Putnam remained stable year over year. Pricing showed notable strength, with the median sale price increasing to $610,000, up 11%. The market continues to benefit from buyers seeking greater affordability relative to Westchester, keeping upward pressure on prices.

Dutchess recorded modest growth, with home sales increasing 3%. Pricing trends were similarly strong, with the average sale price exceeding $600,000, up 9%, and the median price reaching $500,000. Inventory remains tight overall, though trends vary by price segment.

“Looking ahead, the market is expected to remain competitive,” said Liz Nunan, president and CEO of Houlihan Lawrence, the market leader north of New York City. “Without a meaningful increase in supply, prices are likely to continue trending upward.”

The backstory

While sales and pricing have often performed inversely, they have both ridden a roller-coaster in recent years, Construction Coverage noted in its report.

During the Covid-19 pandemic, home values soared, with year-over-year price growth peaking at 26.3% in May 2021 before gradually slowing. By late 2022, annual growth had fallen to just 1%, and by April 2023, prices had declined 4.1% from the previous year. After a period of growth in 2024 and recovery to historical norms, price growth has since cooled. As of January 2026, home prices were just 1.1% higher than the year prior.

While price growth is no longer as extreme, continued demand and limited inventory have kept upward pressure on home prices. Recent data suggests that even as affordability challenges persist, home prices continue to rise, albeit at a much more sustainable rate.

The pandemic initially brought transactions to a near standstill, with sales plummeting by more than a third from the spring of 2019 to the spring of 2020. When the market rebounded, sales surged, reaching a record 48.4% year-over-year increase in May 2021. However, as mortgage rates rose and affordability worsened, sales volume declined sharply, falling 35.1% year over year by December 2022.

Since early 2023, home sales have gradually recovered. Though still below pre-pandemic levels, sales were down just 7.1% year over year by the close of 2023, marking a significant improvement from the previous year’s steep declines. While that momentum continued into 2024, the market has since slowed. As of January 2026, home sales were down 8.3% compared to the year prior.

Where Construction Coverage has seen a cooling off is in Southern and Mountain West markets. In 2021, Texas cities like Arlington, Fort Worth and Austin ranked among the top 15 hottest markets. However, entering 2026, those same cities have dropped into the bottom 15 of the rankings. Similarly, Phoenix and Mesa, Arizona, which were among the most in-demand real estate markets during the pandemic, now rank near the bottom. The rapid home price increases in these regions – combined with rising mortgage rates, inflation and return-to-office mandates — have made these once-popular migration destinations less attractive to buyers.

Affordability remains a major hurdle, especially for first-time buyers contending with high borrowing costs and limited supply in the entry-level segment, especially in the Northeast and California —challenges that have prompted some markets to focus on expanding access to more affordable housing options. As home owners and aspirants move into the prime spring and summer selling seasons, Construction Coverage expected that real estate activity will be top of mind, with certain metro areas emerging as particularly hot markets due to strong job growth, demographic shifts and continued demand for housing.