Tax policy in flux affects Main Street

Eventually, Main Street USA feels the repercussions of corporate tax avoidance practices, but lately those effects have become more uncertain.

“Taxes are reflective of our lives, our politics and real economic realities,” said Helen Mangano, a securities and finance lawyer in Bronxville.

While there is broad agreement that tax avoidance strategies are harming the economy, political gridlock in Washington has stalled efforts to address the problems.

The consequences can be seen with Pfizer Inc., the New York City-based pharmaceutical company that produces vaccines and operates a large research and development center in Pearl River in Rockland County.

Pfizer was in the process of acquiring Allergan Plc, a drug maker based in Dublin, Ireland, for $152 billion. That merger collapsed after the U.S. Treasury issued regulations on April 4 that made the transaction unattractive.

The Pfizer-Allergan deal would have been the biggest ever tax inversion, a controversial but legal technique that corporations use to lower their tax bills.

Pfizer”™s plan was to reincorporate in Ireland, essentially relinquishing its U.S. “citizenship.”

Individuals who give up citizenship still have to pay U.S. taxes for ten years, Mangano said. Not so with corporations.

In the typical inversion, the corporation takes advantage of a lower foreign tax rate by establishing its home abroad, on paper, while continuing to manage and control the company from the U.S.

Inversions often use a related strategy called “earnings stripping.” The foreign-controlled corporation loans money to its U.S. subsidiary for operational expenses. Interest payments are deducted from overall earnings and are not taxable.

The U.S. taxes American corporation profits wherever they are earned in the world. But the foreign earnings are not taxed until they are returned to the U.S.

So American corporations are holding more than a trillion dollars in earnings offshore, to delay or avoid paying U.S. taxes.

The Treasury issued a temporary rule making it harder for an American company to reincorporate abroad. It also proposed a rule that would classify foreign loans to American subsidiaries as equity instead of debt, removing the tax deduction.

“Predictably, Washington is trying to address symptoms without really dealing with the serious underlying issue,” said Ralph Kessler, a corporate and securities lawyer for Hinman, Howard & Kattell Attorneys in White Plains, and an adjunct professor at Hagen School of Business at Iona College.

“U.S. tax policy is out of synch and not competitive with the rest of the world,” he said.

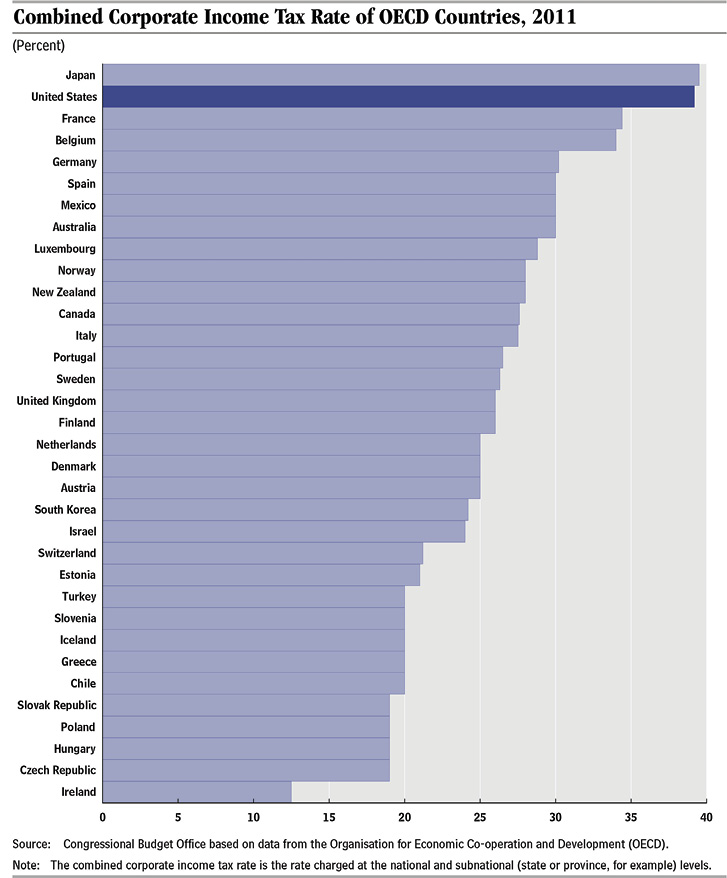

The top corporate tax rate in the U.S. is 35 percent. The average tax rate among developed countries in the Organization for Economic Cooperation and Development, excluding the U.S., is about 29 percent. Ireland”™s corporate rate is 12.5 percent.

Critics of the high tax rate say it distorts corporate investment decisions. Foreign corporations are less likely to invest in the U.S. American corporations are more likely to invest overseas. The Treasury and state governments get less tax revenue.

If corporations could bring back foreign earnings at a lower tax rate, Kessler said, “they could expand here, there would be more jobs and the economy would grow faster.”

Treasury was right to curtail inversions, said Philip G. Cohen, a retired vice president of tax at Unilever United States, and an associate professor of taxation at Pace University Lubin School of Business. Congress has failed to act, he said, and the government had to send a message to stop an abusive tax avoidance practice.

He said the high corporate tax not only hurts U.S. companies with global operations, it burdens smaller U.S. companies that don”™t have foreign operations to use for tax avoidance techniques.

The proposed rule that would treat a company”™s foreign debt as equity goes too far, he said. But putting an end to taxation of foreign earnings of American corporations, as some reformers have advocated, would encourage companies to move jobs and investments outside of the U.S.

“If Singapore decides to offer a tax holiday,” Cohen asked, “why would you put up an R&D facility in Tarrytown?”

“I want to encourage investments in the U.S. I want to make the U.S. business friendly, while at the same time curtailing abuses.”

The Treasury rules have been characterized as stopgap measures to slow down the pace of inversions. There is widespread agreement that comprehensive tax reform is needed.

Cohen said the tax base should be broadened and the statutory rates lowered. But he has written elsewhere that there is little appetite in the current Congress to change a tax system that opens the campaign donation spigot. Maybe next year, if a Democrat is elected president and Democrats control the Senate, a reform bill can be negotiated with a Republican House.

Kessler said neither Democrats nor Republicans can vote for something that helps big business in this election year. After the election, he thinks the two parties might be able to work on tax reform.

“That”™s politics,” he said.