Norman G. Grill: Beware the new tax code’s fringe benefits’ limitations

This year, many businesses will begin enjoying substantial tax relief under the Tax Cuts and Jobs Act (TCJA). For 2018 and beyond, the top corporate tax rate has been slashed from 35 percent to 21 percent. And qualifying pass-through entities (partnerships, S corporations, LLCs and sole proprietorships) are entitled to deduct up to 20 percent of their business income.

At the same time, however, the law offsets some of these tax savings with new deduction limits for certain fringe benefits, including employer-provided meals, entertainment and transportation. To fully understand the TCJA”™s impact on your business, it”™s critical to evaluate the deductibility of these benefits.

Meals and entertainment

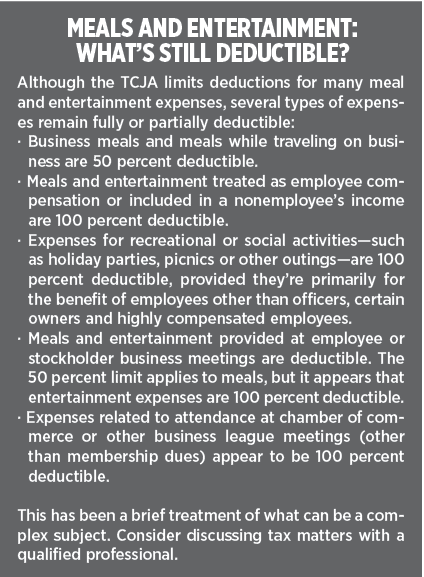

Prior to the TCJA, taxpayers were generally permitted to deduct 50 percent of business-related meal and entertainment expenses. The act retains the 50 percent deduction for business meals (including employee meals while traveling), but it eliminates most deductions for 1) activities considered entertainment, amusement or recreation, 2) membership dues for clubs organized for business, pleasure, recreation or other social purposes, or 3) facilities (or portions thereof) used regarding the above ”” though exceptions exist. (See sidebar “Meals and entertainment: What”™s still deductible?”)

In some cases, the line between deductible meals and nondeductible entertainment may be blurred. For example, is the separate cost of a meal at a sporting event deductible if substantial business is discussed? Further guidance may be necessary to answer that question.

The TCJA also limits (and eventually eliminates) deductions for employer-provided meals that previously were fully deductible as “de minimis” or “for the convenience of the employer” fringe benefits. These include meals provided so employees can work overtime, meals furnished on or near the employer”™s premises and certain expenses associated with operating on-premises eating facilities. The act reduces these deductions to 50 percent through 2025 and then eliminates them altogether. It doesn”™t affect the exclusion of these benefits from employees”™ income, however.

The TCJA also limits (and eventually eliminates) deductions for employer-provided meals that previously were fully deductible as “de minimis” or “for the convenience of the employer” fringe benefits. These include meals provided so employees can work overtime, meals furnished on or near the employer”™s premises and certain expenses associated with operating on-premises eating facilities. The act reduces these deductions to 50 percent through 2025 and then eliminates them altogether. It doesn”™t affect the exclusion of these benefits from employees”™ income, however.

Transportation benefits

Prior to the TCJA, employers were permitted to deduct the expense of qualified transportation fringe benefits (QTFBs) and employees could exclude these benefits from their wages, up to a monthly cap. QTFBs include qualified van pools, qualified parking at or near the workplace, transit passes, and qualified bicycle commuting reimbursements. Employers could also arrange for employees to purchase QTFBs with pretax dollars through salary reductions.

The TCJA disallows employer deductions for expenses, payments or reimbursements for 1) QTFBs and 2) employee travel between home and work, except as necessary to ensure employee safety. According to a recently revised IRS publication, deductions are disallowed whether benefits are paid directly, through a bona fide reimbursement arrangement or through a compensation reduction agreement.

Employees may continue to exclude QTFBs (other than bicycle reimbursements) from their wages (up to $260 per month in 2018). The $20-per-month exclusion for qualified bicycle commuting reimbursements is suspended from 2018 through 2025. During that time, employers may deduct those reimbursements. Beginning January 1, 2026, bicycle reimbursements will be nondeductible by employers and excludable from employees”™ wages.

Next steps

All businesses should review their benefits programs and expense reimbursement policies with respect to these changes. Even if deductions have been reduced or eliminated, it may be possible to obtain a 100 percent deduction for meal or entertainment benefits by including them in employees”™ wages. You might even consider raising employees”™ compensation to cover their tax increases. In addition to those discussed above, the TCJA also limits tax benefits for employee achievement awards, moving expenses and on-site gyms.

Most businesses will likely continue to provide fringe benefits, regardless of deductibility, as an employee retention tool or, in the case of certain transportation benefits, because they”™re required by local law. Nevertheless, it”™s important to understand how the TCJA affects the tax costs associated with employee benefits and to modify your payroll and other systems to ensure that fringe benefit expenses are reported properly for tax purposes.

Norm Grill (N.Grill@GRILL1.com) is managing partner of Grill & Partners LLC (GRILL1.com), certified public accountants and consultants to closely held companies and high-net-worth individuals, with offices in Fairfield and Darien, 254-3880.